2-month surge of 44%, US software stocks are "making a comeback"! Is Chinese internet the "APAC version of IGV"?

```

U.S. software stocks are experiencing the strongest rebound in twenty-five years, going from being heavily neglected to universally sought after. The speed and intensity of this rotation have caught the market off guard.

Since its April low, the iShares Expanded Technology Software ETF (IGV) has risen about 44% in total, and in the past two trading days, it recorded its largest single-day outperformance relative to the S&P 500 since 2001.

In the options market, IGV call options trading volume broke through 280,000 contracts in a single day, setting a historic record, with retail funds also flowing in at record levels. According to data from JPMorgan positions, the software sector’s long-term position is still at the 1st percentile in history—the implication is that the short squeeze is far from over.

Meanwhile, China’s internet sector surged 5% in a single day, prompting investors to ask: Will it replicate the "catch-up" logic of U.S. software stocks? JPMorgan APAC strategist Matthew See believes that although the narratives are similar, there are fundamental differences in profit trends and business models between the two, making simplistic comparisons risky.

IGV’s Historic Rebound: From Ignored to Frenzied Buying

For most of the AI investment boom, semiconductors led the pack, while the software sector was almost ignored. This landscape has been completely overturned in the past few weeks.

According to tracking by The Market Ear, IGV has rebounded about 43% to 45% from its April low to now, almost matching the gains of the Philadelphia Semiconductor Index (SOX) over the same period—this came as a surprise to many investors betting on "chip dominance over software". In recent trading days, software’s excess returns over semiconductors have hit their highest in more than 25 years.

The response in the options market has been particularly extreme. According to Goldman Sachs, IGV call options trading volume broke through 280,000 contracts last Friday, the highest ever single-day volume; Monday followed with 225,000 contracts. Meanwhile, per Vanda Research, retail investors bought $46 million in IGV in a single day, about 40% higher than the previous record set in February.

Three Catalysts: Profits, Narrative, and Short Squeeze Resonate

In early 2026, the sweeping "SaaSpocalypse" (SaaS apocalypse) panic dominated the software sector. Whenever Anthropic or OpenAI released a blog about AI-driven productivity gains, tens of billions in market cap would evaporate from related software stocks, with sub-sectors like legal software also hit and short reports flooding in. Now, all of that is history.

Snowflake’s earnings report was the first spark. After market close on May 27, Snowflake released its earnings, with shares jumping 36% the next day. The surge was driven not only by stronger-than-expected guidance, but also a $6 billion contract signed with Amazon Web Services. The key signal: Snowflake reported significant resurgence in client demand for its AI-powered tools, reinforcing the narrative that "software companies are AI beneficiaries, not victims," and giving IGV sustained buying momentum.

Jensen Huang’s remarks were the second spark. On June 1, at Computex, Jensen Huang directly addressed concerns about AI replacing software companies: "Many people say, with AI agents coming, all software companies will collapse. I say, quite the opposite, because there will be so many agents. The world is no longer limited by people, so these agents will use more tools than ever before." This endorsement from the core of the AI ecosystem gave the software sector’s recovery narrative its highest validation, and IGV rose another 6% that day.

The short squeeze is the third spark. During the "SaaSpocalypse", massive short positions built up in the software sector. As prices rebounded sharply from multi-year lows, shorts were forced to cover, amplifying upward momentum. Retail money flooded in—as per Vanda Research, retail investors’ net single-day purchases of IGV hit $46 million, about 40% higher than the historic record.

Positioning Lows and FOMO: The Short Squeeze Logic Isn’t Over

The key to understanding this rally lies in grasping the sector’s previously extreme positioning structure.

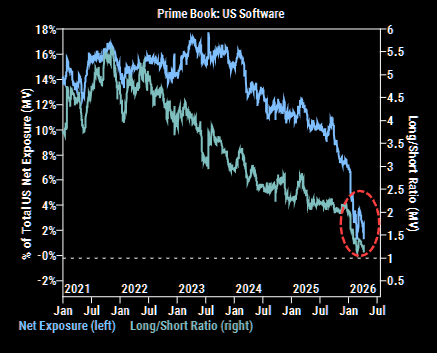

JPMorgan’s position intelligence team shows that the software sector’s long-term positions are at the 1st percentile historically, while semiconductors are at the 97th percentile. Goldman previously noted that the U.S. software sector’s exposure had evolved into "extreme collapse."

This extremely under-owned status means any shift in sentiment can trigger intense catching-up flows. Actual trading behavior shows FOMO (fear of missing out) is spreading to individual stocks. According to Vanda Research, Hewlett Packard Enterprise (HPE) became the second largest retail buy yesterday—it had never appeared on Vanda’s retail leaderboards before. Retail buy volumes in HPE over the past two trading days were equal to total buys over the past 11 months, and HPE’s weekly implied volatility surged.

China Internet: Asia-Pacific’s IGV or a Flawed Comparison?

The strong performance of U.S. software stocks quickly brought attention to another sector across the Pacific.

The Hang Seng Tech Index (HSTECH) recently jumped nearly 5% in a day, broke above its downtrend line, and climbed above its 100-day moving average, breaking out of a months-long triangle consolidation. Leading stocks: Tencent surged 10% in a day—according to a previous Wallstreet article, the market’s expectation for Tencent embedding AI agents in WeChat rose; Meituan jumped 9%, encouraged by signs of a cooling subsidy war in food delivery.

JPMorgan’s research report positions China internet as the "Asia-Pacific version of IGV." Given the intensity of the software short squeeze, if investors embrace a similar catch-up narrative, the moves could be equally violent. Data shows, measured by JPMorgan’s China Internet Basket (JPCHINTE), the sector is down about 15% year to date, almost flat for the past two months, lagging the broad market. Hedge funds have added positions over the past 20 trading days, but total positions are still at the 38th percentile since 2018.

However, JPMorgan clearly warns of fundamental limitations in comparing IGV and China internet: First, IGV companies’ EPS trends are strong through 2026, but China internet sector’s EPS has been almost flat for two years; Second, the business models are fundamentally different—U.S. software companies and Chinese internet platforms cannot be directly compared. He notes this IGV rebound is essentially driven by sentiment reversal, not profit acceleration; for China internet to turn a short squeeze into sustained gains, it will need substantial improvements in EPS trends or clarity in the AI-driven growth narrative—"betting on a growth inflection point is much harder than following an already operating narrative."

Caution on Overbought Signals: The Squeeze Has Arrived, Profit-Taking is Preferable

Amid exuberant sentiment, some market watchers are warning of near-term risks.

The Market Ear notes the current level of overbought in the software sector is extremely rare, similar only to the peak at the end of 2024. IGV is now approaching a key resistance region, and while the institution maintains a constructive view, it clearly states "won’t add new longs right now" but prefers to lock in some gains while rolling calls up to higher strikes to preserve upside exposure.

From a longer-term perspective, the software sector’s strength appears more as a "rebound" in historical charts rather than a trend reversal. The core question is: After this historic short squeeze, how much room is left for catch-up trades? The answer depends largely on whether software companies can translate the AI narrative into visible profit growth.

Risk Disclosure and DisclaimerThe market involves risk and investments require caution. This article does not constitute personal investment advice and does not consider individual users’ specific investment objectives, financial situation, or needs. Users should consider whether any opinions, views, or conclusions in this article suit their unique circumstances. Responsibility rests with the user for investing based on this article. ```